Today, give a try to Techtonique web app, a tool designed to help you make informed, data-driven decisions using Mathematics, Statistics, Machine Learning, and Data Visualization. Here is a tutorial with audio, video, code, and slides: https://moudiki2.gumroad.com/l/nrhgb

![]()

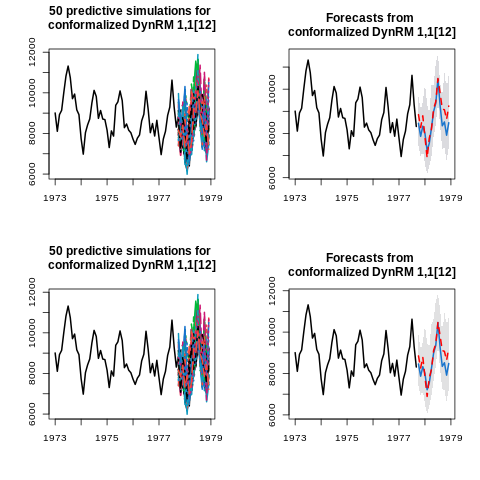

Predictive simulation of time series data is useful for many applications such as risk management and stress-testing in finance or insurance, climate modeling, and electricity load forecasting. This (preprint) paper proposes a new approach to uncertainty quantification for univariate time series forecasting. This approach adapts split conformal prediction to sequential data: after training the model on a proper training set, and obtaining an inference of the residuals on a calibration set, out-of-sample predictive simulations are obtained through the use of various parametric and semi-parametric simulation methods. Empirical results on uncertainty quantification scores are presented for more than 250 time series data sets, both real world and synthetic, reproducing a wide range of time series stylized facts.

Comments powered by Talkyard.